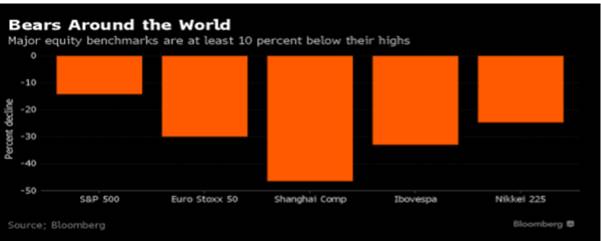

Markets: looking a bit healthier

Equity prices have hitherto in 2016 been driven by herd-like panics over earnings interspersed with hopes of succour from central banks. This has been making markets look depressingly like the Risk On /Risk Off years from 2009 to 2014. Now, however, there are signs of greater discrimination, which if they persist will surely make markets healthier. It is true that all the main indices moved higher last week but not uniformly and with some reversals of over-sold positions, including in Emerging Markets. Even better was that stocks within the various indices did not all move together. It is still too early to call a major change but I was interested to alight on Chart 2 indicating that investors may indeed be more open-minded than they have been in the last few weeks.

It is possible that many investors have finally concluded that central bankers can no longer help them much and that some members of FOMC and MPC do not even intend to try beyond keeping official rates lower for longer. Janet Yellen’s marathon testimony in Congress did nothing to persuade investors that there is any prospect of the FOMC hiking four times in 2016. Nor is there much expectation that the FOMC or MPC will venture into negative rate territory. These views are finely balanced in US Treasury and gilt yields, which have fallen significantly so far in 2016 but remain far above EZ and Japanese sovereign yields. Of course, Messrs Draghi and Kuroda are still strutting their stuff but with contrasting results. Mr Draghi, as the buyer of every resort, has managed to push sovereign bond yields ever lower, capped them for potential delinquents Italy and Spain and even hauled Portugal back from the brink. He has had less success with depreciating the euro but is planning another ‘coup’ at the next ECB meeting in March when the Bundesbank does not have a vote under the rota system. Mr Kuroda has an even bigger problem with the yen, which no matter how reckless he gets, is still seen as a safe haven by domestic and foreign investors alike. None of Mr Kuroda, Mr Draghi and their counterparts in Switzerland, Sweden and Denmark seem to consider that negative interest rates might alarm consumers and businesses sufficiently to curtail their spending: i.e. the opposite result to their aim.

Investors coming to terms with low growth and its impact on corporate earnings and interest rates is surely welcome even if some central bankers still they have unlimited ammunition left. We must hope that they continue to discriminate rather than stampede. Nevertheless, markets are likely to remain very difficult for some time, possibly for several years, and I intend to expand on the Daniel Stewart approach at the Private Client Forum on Tuesday February 23rd.

Chart 1: Armed neutrality?

Source: CNN via @Callum_Thomas

The ironies of Brexit

So much commentary already and we face four more months of it! I have already stuck my neck out to forecast that Britain will stay in the EU and even adding there was never much chance it would not. The negotiations have often seemed like a charade with EU leaders obliged to talk tough to their voters and Mr Cameron posturing to keep most Tory MPs at least pretending to be open-minded. However, anyone who has been involved in complex commercial negotiations will recognise the apparent surprise of EU leaders at their own generosity and the grudging caveats of moderate Tories as signs of a ‘good deal’. Time will show that Mr Cameron has achieved fundamental changes not on immigrant benefits but on future EU politics and governance. While this could well turn out to be generally beneficial there is a danger that the deal will add to the current centrifugal forces within the EU.

The economic arguments for and against Brexit remain tantalisingly unquantifiable. The pro-EU Bertelsmann Stiftung and IFO Institutes estimate the best case for the UK would be a 5% hit to GDP vs. 25% from complete (albeit highly unlikely) isolation from the EU. The main factors seem to be:

- Only selective agreements with EU may be possible, especially on Services where Germany amongst others has proved less than wholehearted on creating a single market. France must be tempted to impose constraints on both the City and the UK Motor Industry.

- The more comprehensive the trade agreements (along the lines of Norway and Switzerland) the less scope the UK will have to avoid EU rules. In particular, the EU may insist on the free movement of labour but, of course this would avoid the negative impact on UK GDP if immigration was halted as Brexit campaigners demand.

- Trade pacts with the rest of world will definitely take time even if Brussels comes up with helpful transitional arrangements, with a negative effect economy albeit not necessarily permanently.

- The pound has already weakened which indicates more trouble if the ‘outs’ win the vote in the form of capital flight, which would also affect gilt prices. If the negotiations with the EU go badly then foreign direct investment could also be hit. Longer-term a weak pound could boost exports provided sufficient trade agreements were in place.

Two ironies seem likely to overshadow any economic arguments that the ‘outs’ are likely to put forward. First, the UK’s success outside the EU will depend largely on extended and extensive co-operation of those it seeks to leave behind. Second, the biggest risk to the UK economy is a messy break-up of the EU, which it may well have help to precipitate. These will prove awkward even for the eclectic and colourful prominent ‘outs’ as they seek to convince ‘conservative’ Brits of the need for a change with unquantifiable consequences. Moreover, Mr Cameron has already proved himself the doughtiest of campaigners.

The probability of Brexit apparently rose by at least 5% to 35% when Boris Johnson crossed his personal Rubicon (an allusion he would surely both recognise and deny) but I shall stick with my confident prediction of no Brexit.

Stop Press: The great BoJo (now also known as BoGo!) has managed to weaken the pound, which is really rather extraordinary for someone not in government. He is going to have a lot of explaining to do as he abandons the City of London. His tactic seems to be the classic ‘there is a problem and only I can fix it’. He has almost certainly ‘fixed it’ for Labour’s Mayoral candidate Sadiq Khan at least!