Even by the highest/lowest EMU standards of politicking the Greece situation is getting both more blatant and complicated. Trying to understand what is going on is like peeling an onion only to find a walnut in the middle. Finance Minister Varoufakis seems to be enjoying himself exercising his game theories on his EMU counterparts, the former troika institutions and even his colleagues in Syriza but he is probably on his own in that regard. Perhaps the most intriguing development is his attempt to manipulate the EU Commission (which along with France appears to be actively supporting the Greek cause, including, it is thought, drafting the final letter of agreement) against the IMF and, of course, the Germans.

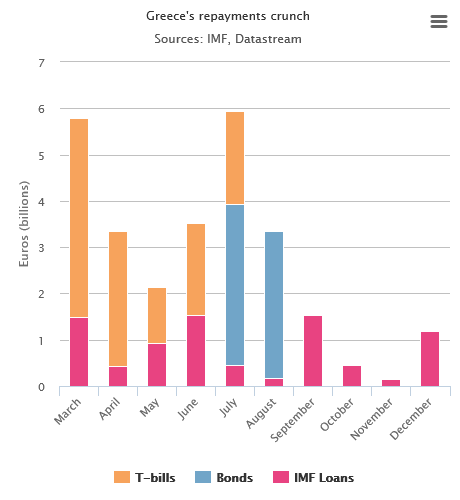

Figure 2. Greece’s Repayments Crunch

One has to assume both Greece and Germany are going for ‘all or nothing’ in another game. The Syriza government seems intent, after all, on seeking unprecedented debt relief from the IMF and the ECB (nothing is due to the EMU bail-out fund until 2023) while sticking to most of its election programme despite promising not to. This is making it more difficult for the EMU federalists to lean on and/or outmanoeuvre the Germans and their allies in the North and (now also) in Iberia. In fact, it is a threat to the whole EMU project as the Germans also seem willing to accept the risk of collateral damage if Grexit were to occur. Mr Schäuble is not as isolated as Syriza say (hope) he is in his insisting that they stick to the bail-out programme as amended by last week’s accord. Nor is he contemplating handing over any new money before June and only after seeing real progress in Greece. (Although over the weekend in the usual confusing EMU way, Jeroen Dijsselbloem, Chairman of the Eurogroup of finance ministers, has hinted that some further emergency money might be made available.) Accordingly, the gaming makes Grexit still seem very possible. In fact, it could be that both Greece and Germany have given up on each other already and are using the next four months to plan the divorce.

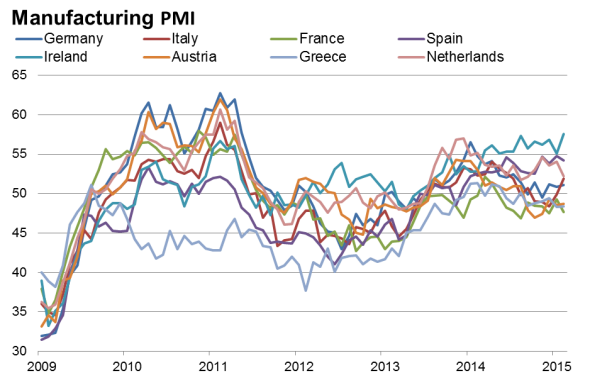

Figure 3. European Manufacturing PMIs

Source: Markit

Meanwhile, there are signs that the EMU economy may have stopped getting worse, which is not the same as a recovery. Yet again, it needs to be stressed that disinflation and deflation boost GDP as they deteriorate and that this has flattered the strong Q4 GDP headline numbers from Germany and Spain. In other data released in February, Germany continues to fare best except for the Manufacturing PMI and Spain is showing the most signs of improvement if one looks beyond Unemployment. Despite the bold talk of reform, France and Italy are yet to report any concrete progress.

This week the ECB announces details of its QE programme, which few people apart from a majority of the Governing Council expect to generate much growth or inflation. At least the Bundesbank is preparing to participate….for now…. and grumbling as it does so. In another provocation to Berlin, the EU commission has granted without offering much explanation extensions to both France and Italy on the timetable to comply with EMU budget deficit rules. Any relaxation of austerity may be helpful for short-term economic activity but the further accumulation of public debt in some countries makes more likely some sort of rescheduling, which is exactly what the Germans fear.

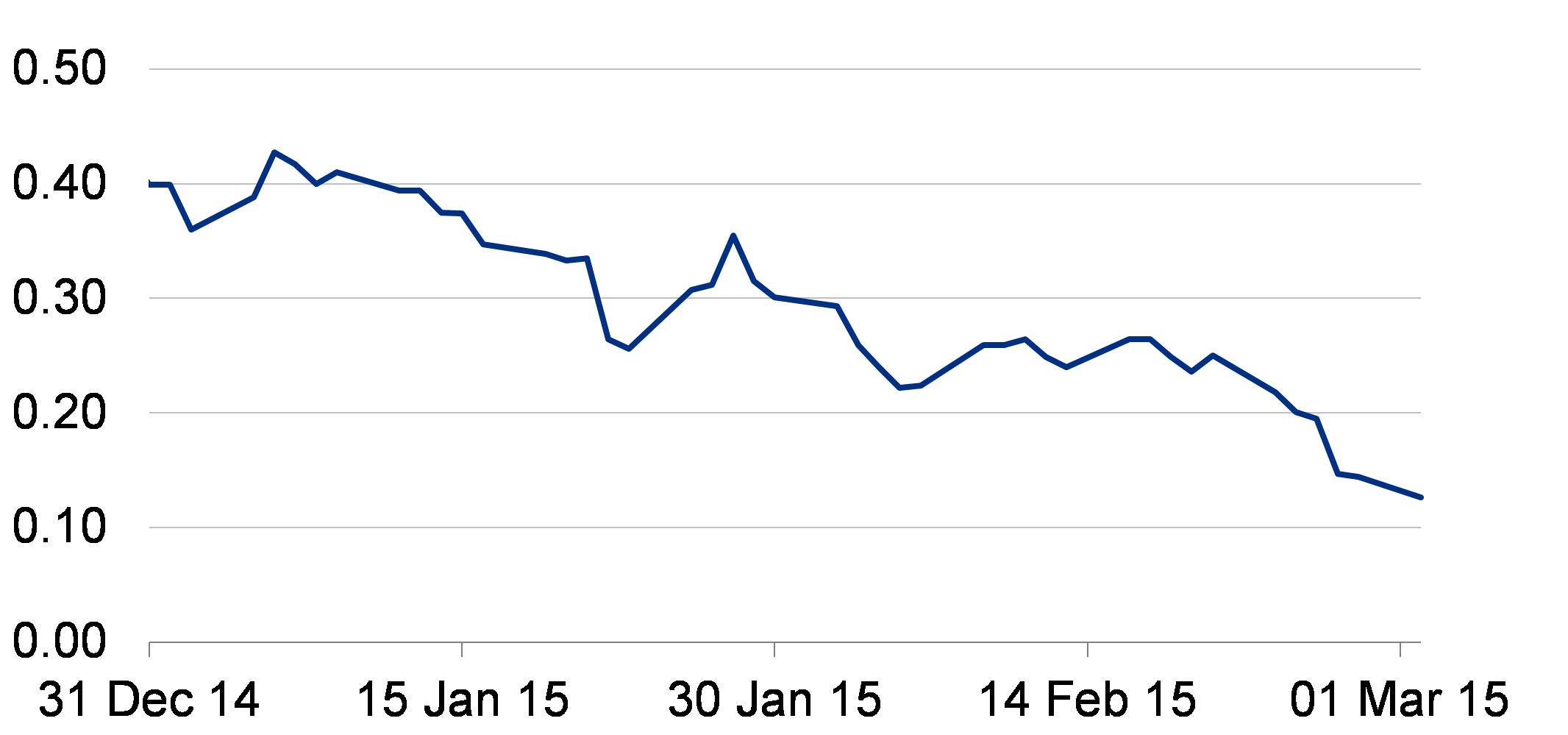

Figure 4. European negative yield club

For now, equity markets are still enjoying the rally that began with expectations of QE but it remains to be seen how much of the proceeds of monthly bond sales remains in Europe. QE expectations have also already taken bond yields into new territory with 30% of them estimated to be negative and, of course, most investors see little risk of EMU break up, even including Grexit. A weaker euro remains the most achievable targeted outcome of QE and, in fact, seems likely in almost every scenario, even if hot money from the US and Japan may get in the way in the short-term.

DAX: Is QE really that good for German companies?

Source: Bloomberg

Two-year Spanish government bond yields:OMG! Might these go negative?

Source: Bloomberg